Insight

Challenging outlook for emerging Asia

KHOON GOH, HEAD OF ASIA RESEARCH, ANZ | JULY 2019

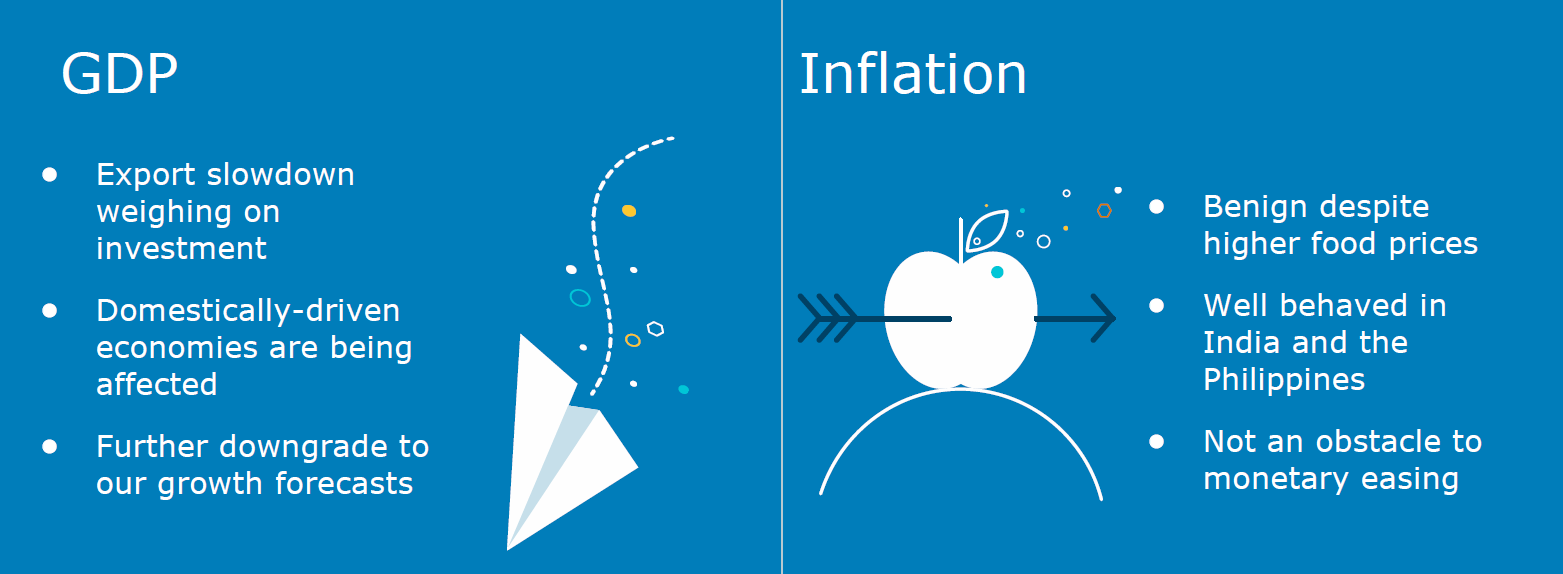

The downturn in the global technology cycle and uncertainty stemming from the US-China trade conflict has had a larger impact on Asia’s economic activity than previously thought. While the region's tech-heavy economies have borne the brunt of external headwinds, idiosyncratic developments are also holding back growth in the region's less export dependent economies.

The contraction in exports has started to feed through into slowing investment activity. At this stage, household consumption is generally still holding up.

With prospects for a recovery likely to be delayed, ANZ Research has cut its gross domestic product growth forecasts for emerging Asia to 5.4 per cent in 2019 and 5.5 per cent in 2020, from 5.7 per cent in both years previously.

ANZ Research has also trimmed its inflation forecasts from already benign levels.

_________________________________________________________________________________________________________

“Idiosyncratic developments are holding back growth in the region's less export-dependent economies.”

_________________________________________________________________________________________________________

Some relief

The current truce between the US and China, agreed at the G20 Osaka summit, is welcome. However, there is no certainty that a longer lasting trade deal can be reached in the coming months. Wider trade tensions look likely to linger for some time.

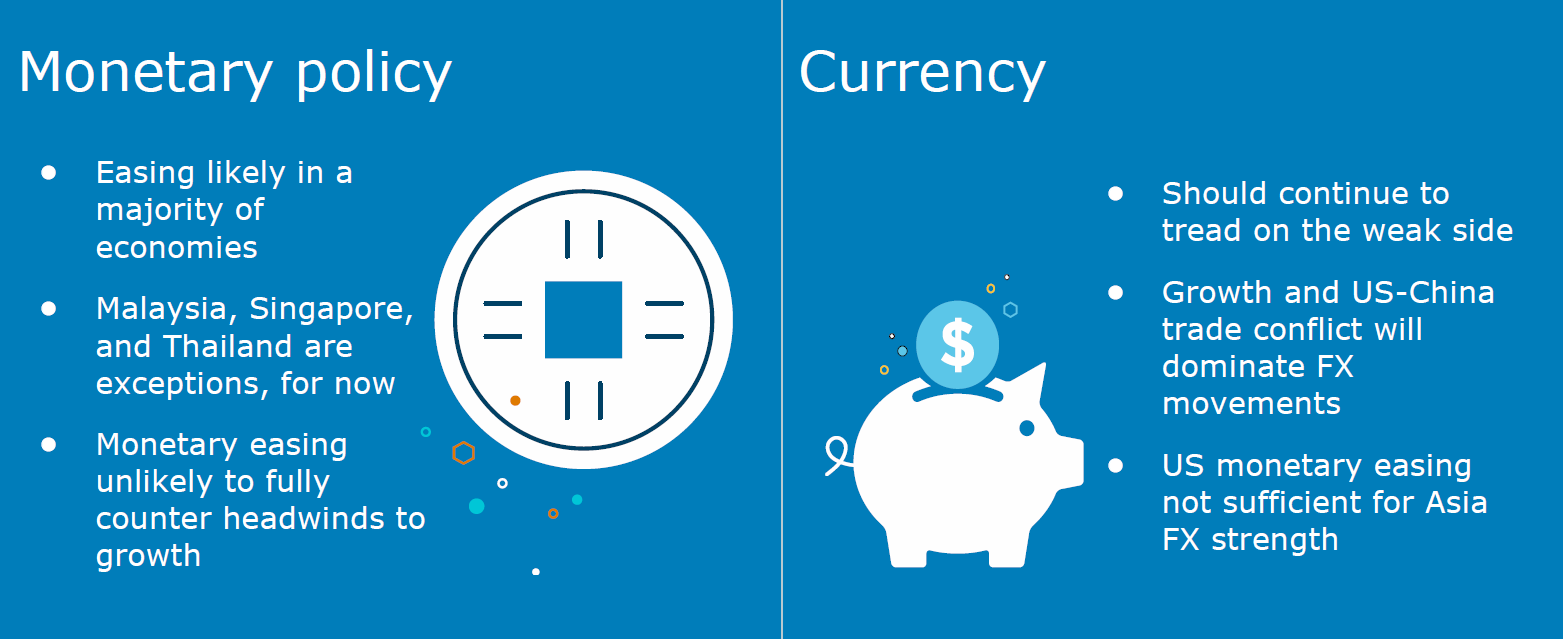

What will help is monetary easing from the US Federal Reserve. ANZ Research expects the Fed to cut the fed funds rate by 50 basis points over the second half of this year, to sustain the economic expansion in the US. Expectations of looser US monetary policy have already helped boost Asian financial markets.

Lower US interest rates will also provide space for Asian central banks to ease monetary policy, without having to worry too much about disruptions to domestic financial markets. So far, the Reserve Bank of India, Bank Negara Malaysia and Bangko Sentral ng Pilipinas have cut their policy rates this year.

ANZ Research expects Bank Indonesia, Bank of Korea and the People’s Bank of China to join in the policy easing later in the year to help support growth.

More can be done

But monetary policy easing by itself will not be sufficient to offset the downside growth risks in the region. Fiscal policy will also need to do some of the heavy lifting.

In this regard, it is only China that has been pro-active in utilising fiscal policy to support growth, while South Korea has announced only a marginally more expansionary fiscal policy with a supplementary budget amounting to 0.3 per cent of GDP.

The fiscal headroom for some economies like India and Malaysia is considerably smaller. In Indonesia, there is scope for an expansionary fiscal policy but this will be dependent on foreign investor appetite for additional bond issuance.

But just as expectations of Fed easing has provided a window for Asian central banks to ease policy, prospects for other major central banks like the European Central Bank and Bank of Japan to also provide additional monetary policy stimulus offers Asia’s fiscal authorities room to undertake a more expansionary fiscal policy.

The search for yield by investors looking to escape negative interest rates in Europe and Japan mean demand for Asian sovereign debt will be strong. Especially if the fiscal policy boost is also accompanied by economic reforms.

Khoon Goh is Head of Asia Research at ANZ

RELATED INSIGHTS AND RESEARCH

insight

Everyone is easing: the outlook for Q3

Trade tension has been a surprising drag on growth and central banks could be called into action. Here are ANZ Research’s forecasts for the second half of 2019.

insight

Australia’s options in the trade war

Continued US-China tensions could be a double whammy for Australia’s GDP – and put a dent in hopes for a return to surplus.

insight

Forget the trade war: ageing is China’s biggest threat

The key to China’s future growth will be its productivity and how it handles its demographic challenges.