INSIGHT

The Evolution of FX Risk Management

Download the PDF

Nicholas Angove, Director, Specialist Funds, FX Sales, ANZ |

Peter Nealon, Executive Director, Institutional, ANZ |

Niamh Targett, Head of Specialty Funds Asia, ANZ |

Robert Tsang, Director, Client Insights & Solutions, ANZ |

February, 2018

________

History shows ignoring FX shifts can prove costly for fund managers – and in 2018 that remains truer than ever, especially for sector-specific specialty funds and long-dated funds that traditionally rely on forwards to manage FX risk.

Developing a measured and consistent hedging strategy should be a key priority for specialty and long-dated funds this year and well beyond, given the expectation the Fed will continue to raise rates in coming months, and the fluctuating outlook for many currencies.

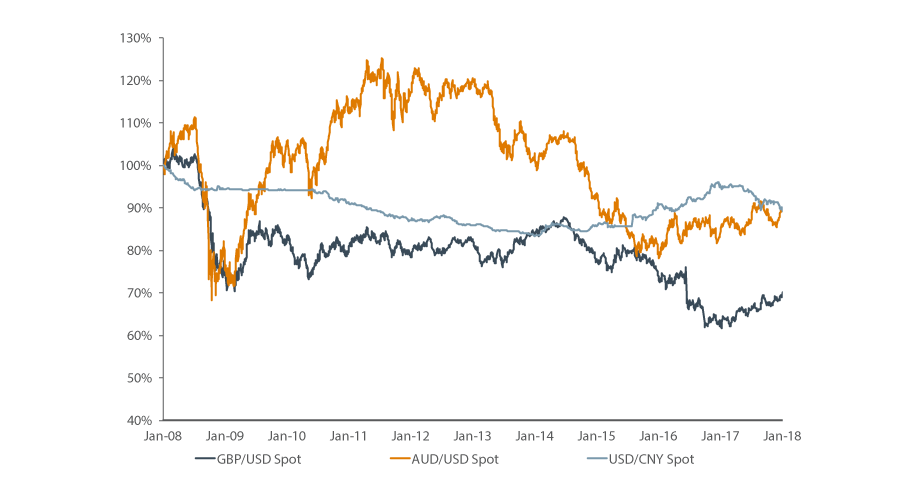

Fund managers need look no further than sterling’s performance in the three years to June 2017 (see graph below), when the sterling-dollar price varied by more than 10 percent each year. Sterling was in a steady depreciation against the dollar and resulted in an overall decline of 25% during the period. Any manager investing sterling in un-hedged dollar assets would struggle to make up that cumulative decline in AUM.

I. Credit Lines and Cost Management

When it comes to managing FX risks in 2018, what should be top of mind for specialty and long-dated funds?

For starters, managers need to understand that robust hedging programmes require ample credit lines. However, many fund managers struggle to obtain credit lines on short notice. That means managers must plan well in advance so they aren’t caught in a pinch following unexpected swings in currency valuations.

Secondly, specialty and long-dated fund managers should commit to an investment ethos that actively guards against a false sense of security. The recent period of low FX volatility has allowed many managers to feel they have little reason to hedge. But if and when volatility does return, it could require substantial credit line increases or, if its effects mean the fund breaches its collateral agreements, the need to put up cash. That could be problematic for specialty funds, many of which are traditionally illiquid.

A third consideration should be achieving a firm grasp on the cost of hedging, particularly for managers based outside developed markets. Long-dated trades in Asia, for example, are relatively costly: a one-year dollar hedge in India might see the client paying away 5 percent; in China it could be 3-4 percent.

A third consideration should be achieving a firm grasp on the cost of hedging, particularly for managers based outside developed markets. Long-dated trades in Asia, for example, are relatively costly: a one-year dollar hedge in India might see the client paying away 5 percent; in China it could be 3-4 percent.

Lastly, managers should structure their funds with a weather eye on the regulatory requirements of different jurisdictions, such as the rules on posting margin should a hedge move against the underlying asset. US and EU funds, for example, need to ensure they don’t fall foul of the variation margin (VM) rules. One solution is structuring the fund to create an offshore hedging entity, which provides greater flexibility when using different solutions such as options and put-call spreads.

II. Devising a Consistent Strategy

When determining a suitable hedging strategy based on the considerations above, managers must also consider the fund’s objective and its liquidity or cash settlement risk. For example, does the fund prioritise stable growth in the NAV in capital currency? Does it demand certainty of earnings? And how should it deal with liquidity or cash settlement risks?

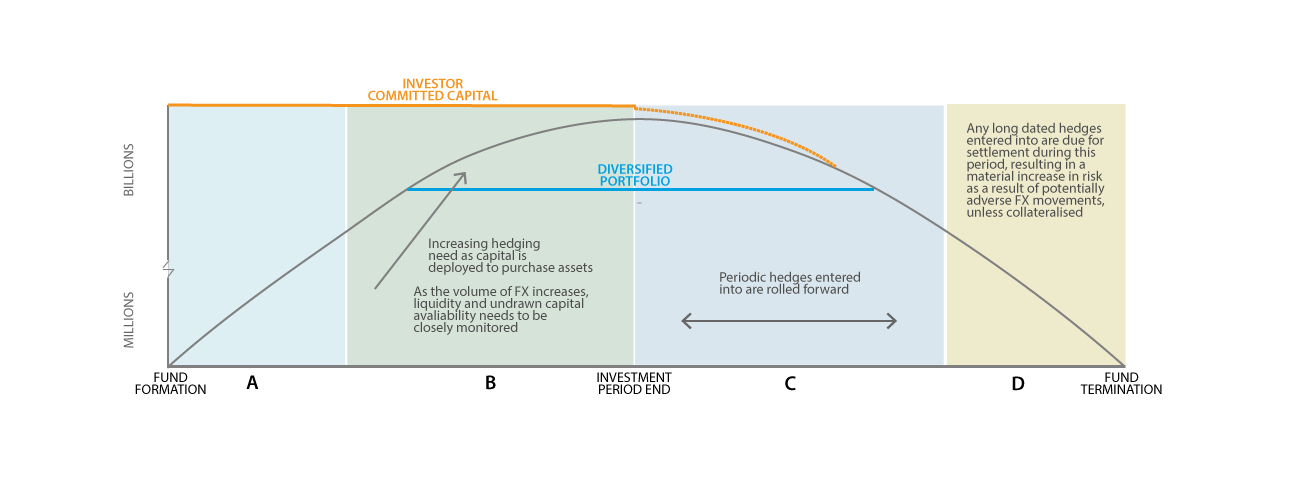

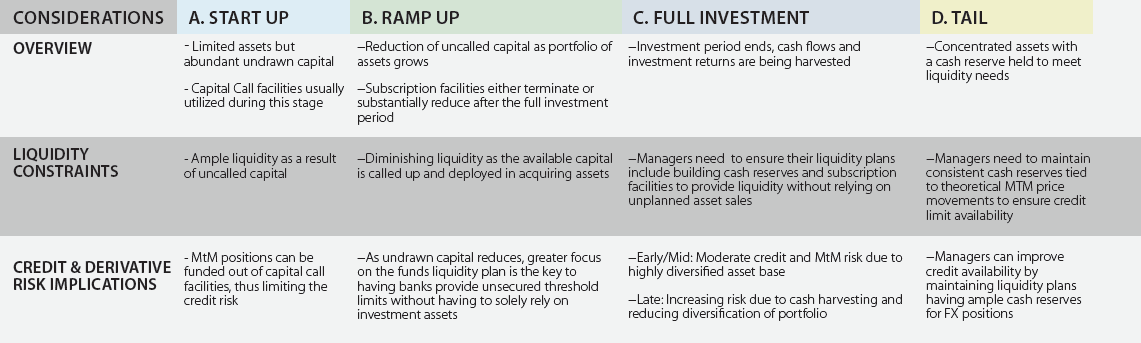

Managers also need to keep in mind that a fund’s liquidity and availability of capital will change over its lifecycle. As a fund moves towards full investment – and later into its tail phase – not only does its effective liquidity shrink, but a growing mark-to-market risk also brings exposure to fluctuations in the value of the underlying assets.

The consequence? The fund might need to provide cash margin or other types of security. That requires forward planning and knowing which hedging products would work best at which stage.

III. Looking Beyond Forwards

Hedges, which are typically an offset to the performance of the underlying asset, can be categorised as either committed hedges or uncommitted hedges. The former provide committed financial obligations; the latter are suitable as insurance for tail risks.

Forwards are more efficient when a foreign currency is expected to weaken; they often provide better earnings and cash settlement outcomes.

If stable growth in the NAV in capital currency terms is a priority, or if earnings certainty is required, a forward might be used. However, although forwards protect from the downside, they require paying away any potential upside. In terms of settlement risk, both the cash outlay and the payoff would be subject to future market conditions.

Part of a manager’s liquidity plan could be to use something other than just FX forwards, such as options structures, and put-call spreads to manage the risk but still position themselves for upside potential.

Bought options provide certainty in terms of cost; however, the payoff is unclear. These are more efficient when there is uncertainty over a foreign currency’s movement. Also, they limit cash outlay, provide protection from downside risk to earnings, allow the benefit from foreign currency appreciation, and boost NAV.

The Cost of Switching Strategies

It is better to stick with a consistent hedging strategy rather than switching mid-stream, because doing that can bring extra costs. Take, for example, Company X, which buys an option at a cost of 2 percent to match its LTV ratio. One year later, after the market has moved in Company X’s favor, the option expires worthless.

The following year Company X decides not to re-hedge its LTV using an option, and instead uses a one-year FX forward. That means deferring the cost – which is now unknown – but, in the immediate term, saving 2 percent. Unfortunately this time the market moves against the company, and the settlement cost of the forward is 5 percent of the notional value of the trade.

In this instance Company X would have been significantly better off using an option for year two as that would have been both cheaper and ensured a fixed settlement risk.

Market conditions such as implied volatility and current forward points are also important in determining the relative cost of options and cost-benefit of forwards respectively.

Finally, managers should ensure that any hedge takes into account the terms of the underlying investment. Using short-dated options or short-dated forwards on long-dated assets will see, in the first instance, a fund paying multiple fees on renewal or, in the second, being exposed to repeated unknown liquidity events. That might or might not prove suitable for the fund’s circumstances, but this ought to be considered.

Of course, these are not the only solutions. One alternative is to use a “natural hedge”, which involves aligning the currencies of the liabilities with those of the assets. Another is to do nothing, and use the FX spot market to convert currencies when needed; however, that leaves all FX risk with the fund and could induce significant performance gaps.

IV. No Perfect Solution

Ultimately the choice of hedging product comes down in part to managing a fund’s scarce liquidity. As always, there is no perfect solution: while using bought options means paying away a premium, using forwards means no upfront cost but the possibility of incurring a risk down the road.

It is worth noting that funds in different parts of the world face different challenges, so what works for a specialty fund manager in Australia won’t necessarily work for one in the US or Europe.

Although every hedge carries a cost, not hedging can end up proving much more expensive.

RELATED INSIGHTS AND RESEARCH

insight

Why It's High Time to Dip into Asia's RegS Liquidity Pool

Rising middle class wealth in Asia has triggered a revaluation of global credit among Asian investors, especially the offshore US dollar bond market. This revaluation has created a deep pool of liquidity across the world's most dynamic region for both issuers and investors.

insight

Are Pan-Asian Corporates Missing the Formosa Opportunity?

In recent years, Taiwan’s ‘Formosa’ bond market – which refers to bonds issued in Taiwan but denominated in currencies other than the New Taiwan dollar – has emerged as a leading offshore fundraising destination. But are pan-Asian corporates taking advantage of the opportunity it presents?

insight

Why Reg-S Bonds Are Booming Down Under

There’s never been a better time for Australian borrowers to raise funds in Asia’s US dollar RegS bond market. The RegS issuance data in Asia speaks for itself - deal volumes have broken records in 2017, up 67% year-on year to US$257bn by mid-November, and this trend was reinforced by the speakers at our recent ANZ Aussie Day conference in Hong Kong.